The following article is from Photovoltaic Industry Research, authored by Yiheng Technology - Yizhikai

HJT's domestic history is mainly divided into five stages:

Phase 1: MW level small batch research and development stage, with a time point from 2013 to 2016. The main manufacturers are Hanergy R&D and Hebei Langfang Xin'ao Film. By the end of 2015, the research and development batch efficiency could reach 23% (double-sided amorphous 5BB pattern);

Phase 2: Pilot batch stage at the hundred megawatt level, taking place from 2016 to 2017. The main manufacturers are Shanxi Jinneng and Taixing Zhongzhi, using MBB (multi main grid) technology to achieve an average production efficiency of over 23.8% and an actual production capacity of around 300MW;

Phase 3: Batch production stage of 200MW-400MW scale, from 2020 to 2022. The main manufacturers are Aikang Technology, Huasheng New Energy, and Tongwei, using MBB matching light injection technology. The cell efficiency can reach over 24.6%, and the actual production capacity is about 2GW;

Phase 4: GW level mass production stage, scheduled for 2022, with main manufacturers including Huasheng Energy, Jingang Photovoltaic, Aikang Technology, Mingyang Intelligent, etc., using single-sided microcrystalline technology matched with VTTO technology, the cell efficiency can reach over 25.3%, and the actual production capacity is 15GW;

Phase 5: GW level mass production stage, starting from April 2023. The main manufacturers are Huasheng Energy, Dongfang Risheng, and Liansheng Technology, using double-sided microcrystalline technology. The average efficiency of the cell can reach 25.5% or more, and the actual production capacity is 35GW.

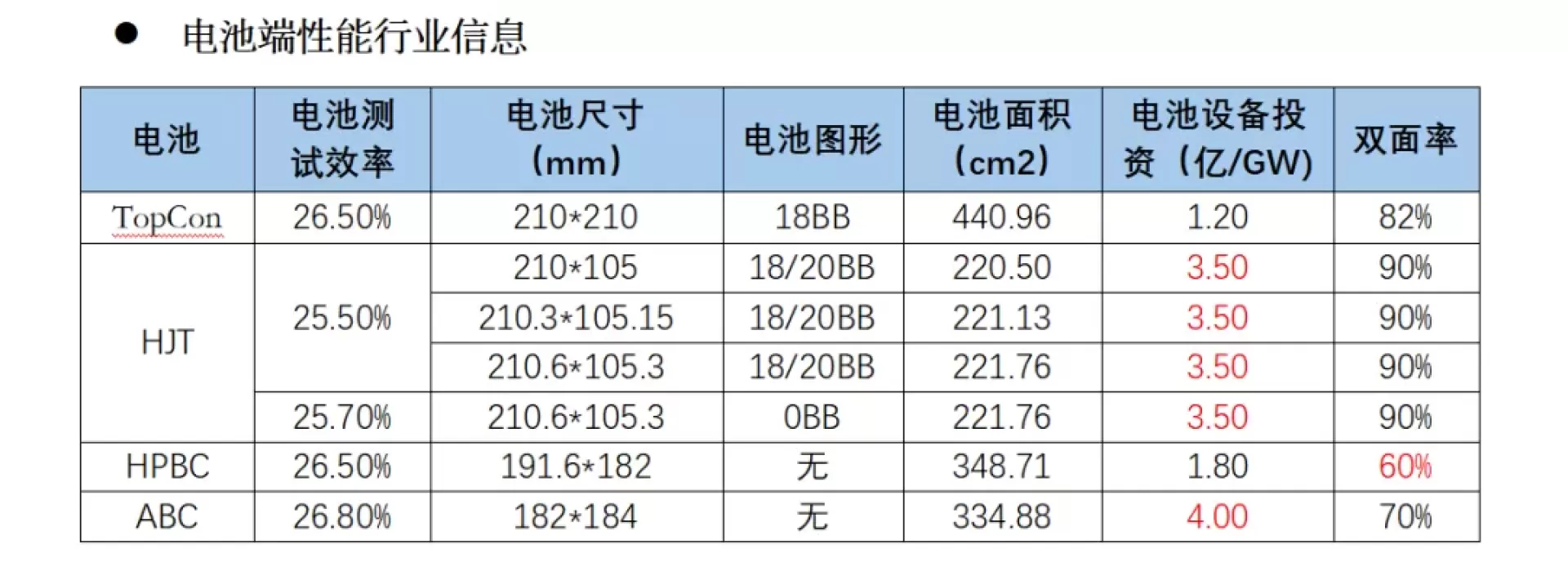

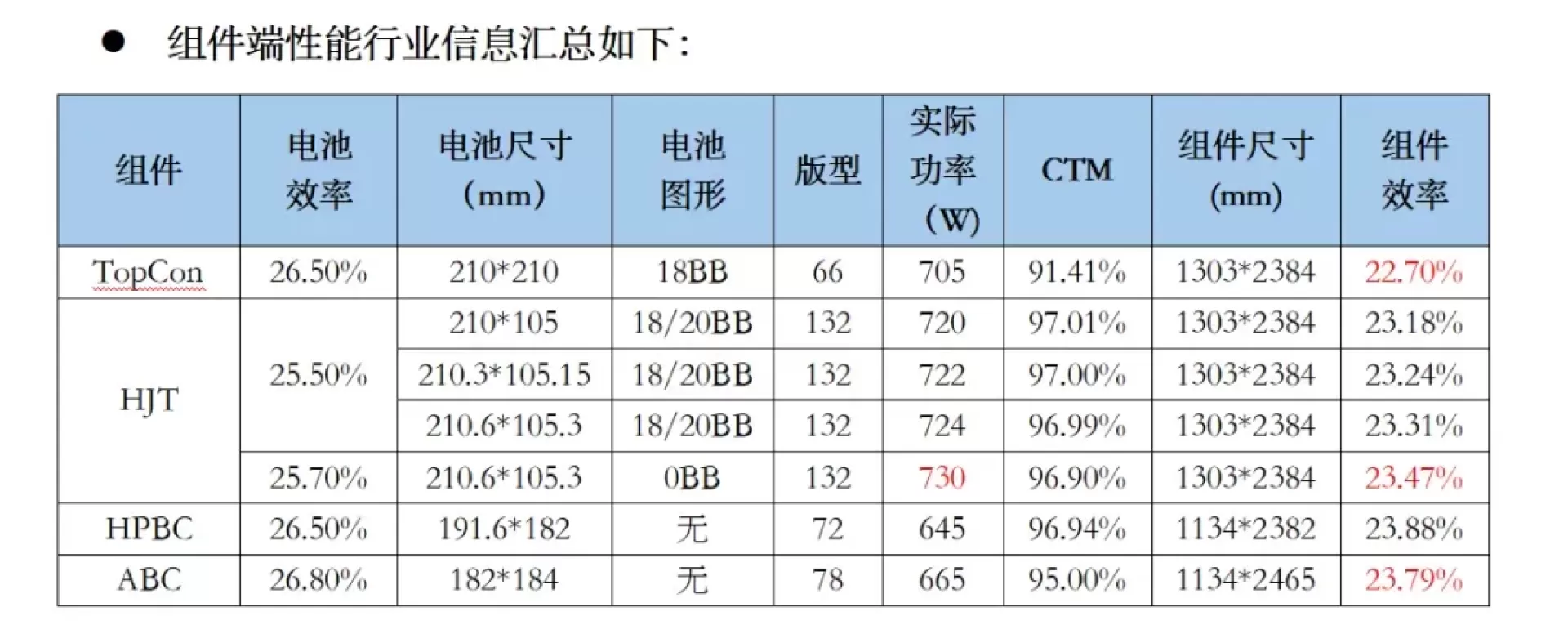

Comparison of current mainstream high-efficiency cell module performance:

The mainstream cells in the photovoltaic industry include TopCon, HPBC, ABC, and HJT. Industry information statistics are as follows:

① Testing efficiency: ABC has the highest efficiency, followed by TopCon and HPBC, while industry HJT cells testing has the lowest efficiency. HJT adopts the ISFH (Hamelin) standard, while other cell testing standards are unknown;

② Equipment investment: HJT is close to ABC cells;

③ Double sided ratio: HJT has a greater advantage, while HPBC cells have the lowest.

① The above standards are based on the latest TUV Rheinland testing standards and are all achievable standards.

② The efficiency of BC cell modules is close to 23.8% (small version modules), leading the module efficiency by 1% and 0.4% respectively compared to the large version TopCon and 0BB HJT.

③ HJT has a significant power advantage on the 210 half chip 132 version, and optimizing the component BOM can achieve 730W. The main factor that reduces the power by 0.4% compared to BC components is Isc (short-circuit current).

Regarding the issue of HJT cell efficiency improvement, the future will mainly rely on improving LSC (short-circuit current):

(1) Back throwing process

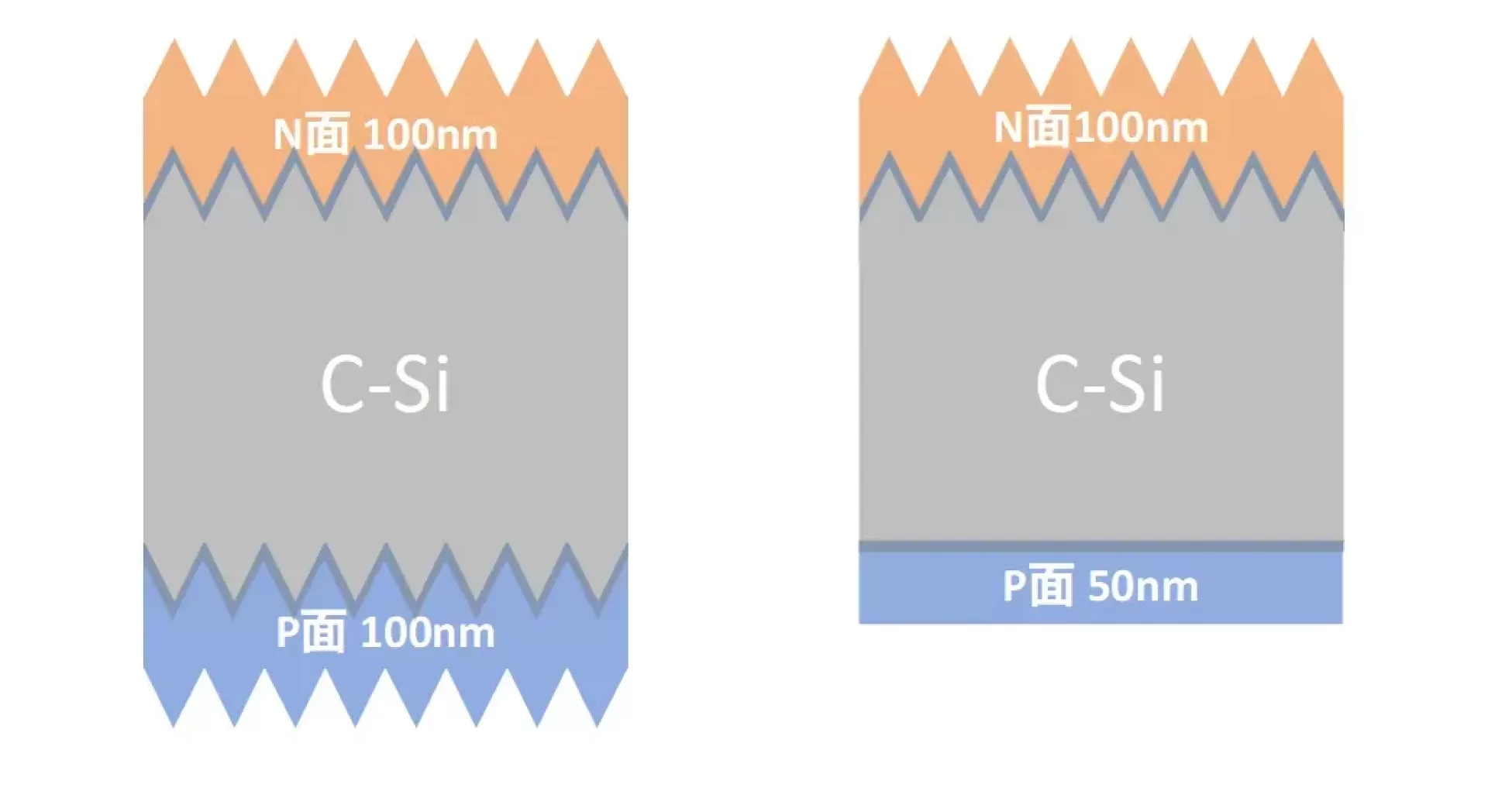

In the cell process, Isc is mainly improved through backside polishing technology, which is expected to increase by 50-60mA. Then, FF is increased by optimizing the thickness of the backside film. The total efficiency of backside polishing is expected to increase by 0.25%, but at the same time, the double-sided rate of the cell will decrease by 10%. In addition, optimizing the back TCO thickness is necessary for back polishing to achieve better efficiency improvement. The back TCO thickness needs to be adjusted from 100nm to 50nm, which is expected to reduce the TCO cost by 0.01 yuan/watt. The structures of HJT conventional cells and back polished heterojunction cells are as follows:

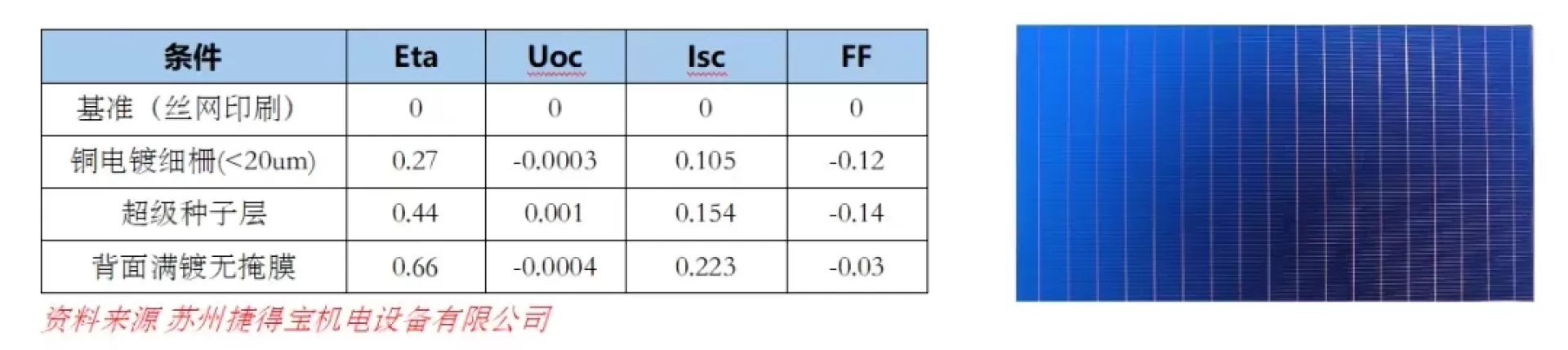

(2) Optimization of metalization line shape

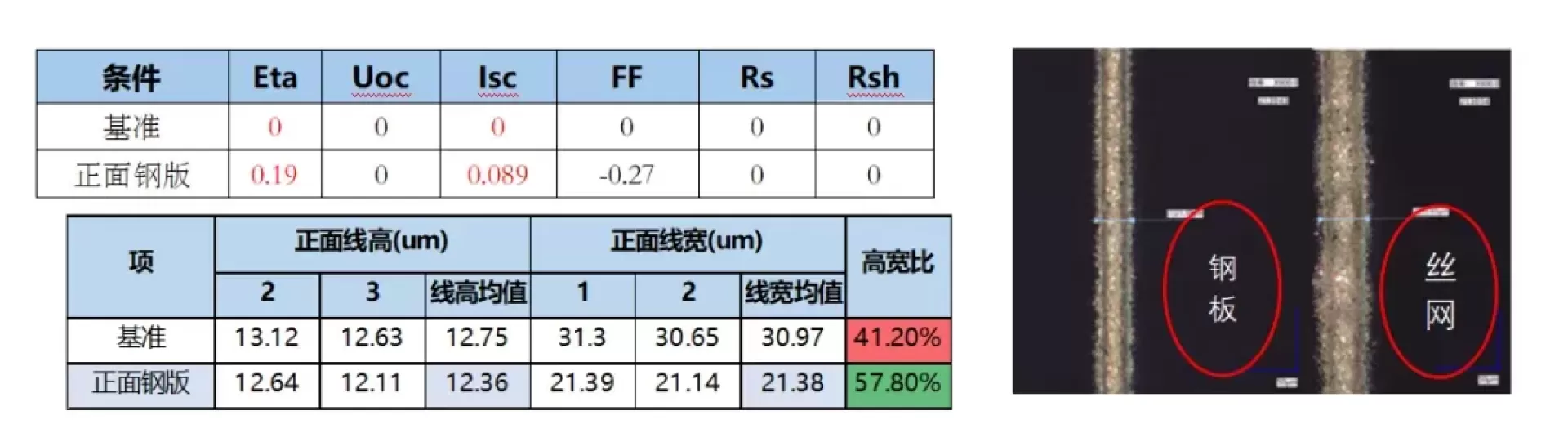

1. Screen printing: Based on traditional screen printing, fine grid lines with a height to width ratio of over 50% can be obtained by optimizing the structure or material of the screen plate. Currently, experiments mainly focus on steel plates and nickel plates, with an expected efficiency improvement of about 0.1-0.2 and an Isc increase of 70-80mA. However, there is a certain loss in FF, and the efficiency improvement brought by steel plates and nickel plates in the industry varies to some extent.

The relevant data for steel plate testing are as follows:

2. Copper electroplating metallization technology, through electroplating metallization technology, obtains finer and higher fine gate lines

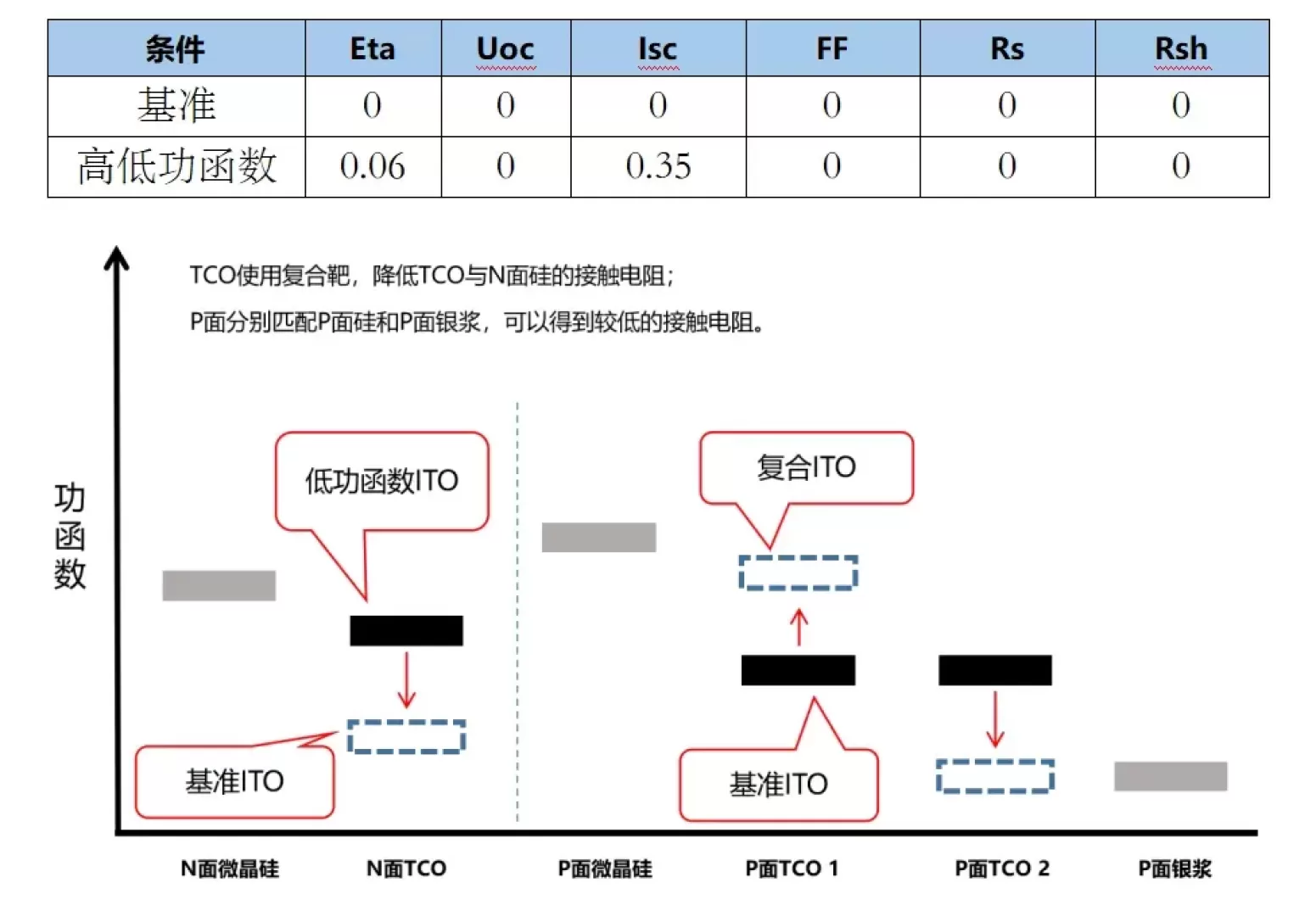

(3) Optimization of TCO work function on the front and back of the cell

The front side adopts a low work function TCO target material (matched with a low work function microcrystalline N layer on the front side), and the back side adopts a double-layer TCO structure (contacting the microcrystalline P layer for high work function and contacting the silver paste for low work function). It is expected to increase Isc by 35mA and efficiency by 0.06%

The data and cell structure are as follows:

Efficiency conclusion:

The back throwing process is expected to achieve stable mass production in the first quarter of 2025, with an expected efficiency improvement of 0.25%. Metalization TCO、 The secondary velvet processing is expected to improve efficiency by more than 0.3%, so that the efficiency of HJT cell 18/20BB cell can approach 26.1%, and the 0BB cell is expected to reach 26.3%. In terms of component efficiency, the 0BB component can easily exceed 24%, and the component power can reach 745W.

In terms of cost:

(1) Nowadays, the non silicon cost of double-sided microcrystalline 0BB silver coated copper HJT cells is expected to be 0.21 yuan/watt. Through the optimization of the back polishing process and the mass production of GW level equipment (depreciation of manpower, water and electricity), the non silicon cost is expected to be reduced to 0.18 yuan/watt, which is very close to the current TopCon non silicon cost of 0.155 yuan/watt. Matching with thin film (130umTopCon, 110umHJT), the HJT cell cost is expected to be reduced by 0.005 yuan/watt, and the final difference between the cell end cost and TopCon will be shortened to 0.02 yuan/watt.

(2) In terms of component cost, HJT's latest centralized procurement price for central enterprises is 0.79 yuan/watt, while BC's is 0.82 yuan/watt. It is expected that HJT will not have any disadvantage compared to BC in terms of cost.

Summary:

(1) In terms of efficiency, the BC component has a huge advantage, leading TopCon component by 1% and HJT component by 0.4%;

(2) HJT does not have too many problems on the cost side, and reducing fixed assets investment and improving efficiency are the most important things at present;

(3) The efficiency improvement of secondary velvet/TCO work function has been achieved in batches on the latest production line, with a total efficiency improvement of 0.15%; The back throwing technology has been validated in Isc improvement and is currently in the process of optimizing the contact resistance of the back paste. It is expected to be introduced into mass production in March 2025, with an expected efficiency improvement of 0.25%; Steel/nickel plate printing technology has been widely adopted in some enterprises, with a large-scale efficiency improvement of over 0.1%. The comprehensive HJT can be increased from the current 25.5% to 26%, which is relatively reliable;

(4) The standalone 1GW equipment on the device side will be tested and completed in the second quarter of 2025, and the equipment investment will be further compressed, expected to be between 250-300 million/GW.

In the short term, it can be seen that HJT efficiency can match the current BC, and the large-scale equipment on the cost side will also bring about a significant decrease in costs. Compared to BC equipment, it is still slightly more expensive, but it still maintains a significant advantage in component power and double-sided ratio.